When can I retire and how long do I need to save before I can retire?

That’s the key question! This interactive fire calculator was built to let you play with the inputs and help you understand how savings rate and retirement spending strongly determine how long it will take you to save up for retirement. Note: it does not simulate the post-retirement period when you start to draw down your savings. That can be done on this post-retirement fire calculator (Rich, Broke or Dead) which compares the frequency of various outcomes in retirement (running out of money, ending up with way too much money, and life-expectancy).

– Use this button to generate a URL that you can share a specific set of inputs and graphs. Just copy the URL in the address bar at the top of your browser (after pressing the button).

Ever since I read Mr Money Mustache’s blog, I’ve been creating spreadsheets dealing with early retirement. I wanted to create a tool that would be accessible to everyone and provide a useful and educational visualization of the process in addition to crunching the numbers.

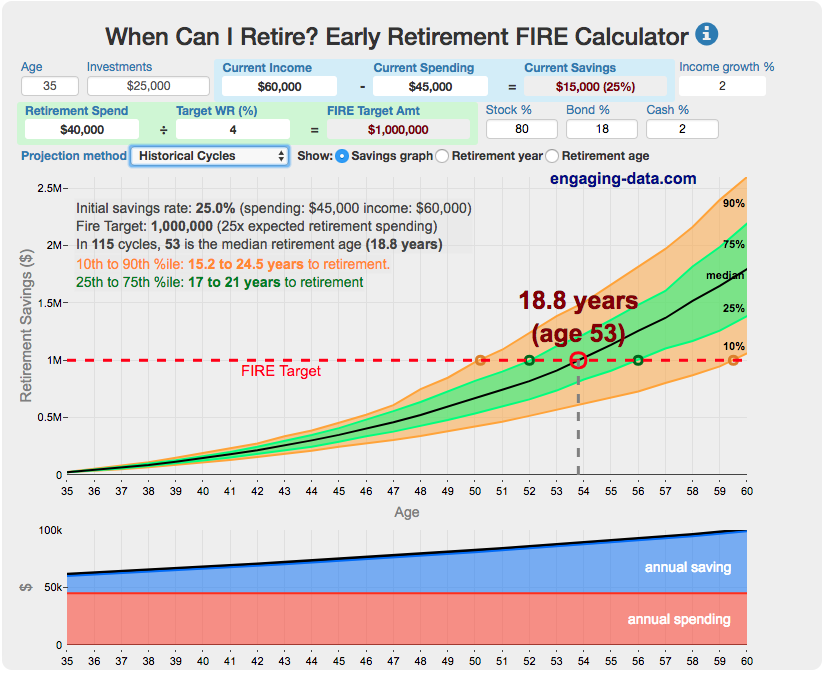

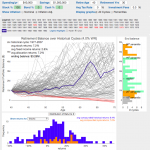

This early retirement fire calculator / visualizer is designed to project the number of years until you can retire, based upon a few key inputs such as annual income and spending, income growth rate, expected annual spending in retirement and asset allocation. It is a pre-retirement calculator that is useful before you retire to get a sense of how many years it is likely to take to accumulate enough money to retire. The three primary modes that are available in the early retirement calculator are: (1) constant, single fixed-percentage real return rates, (2) historical series of real returns are applied to account for likely variability in future returns and (3) monte carlo simulation of the variable returns based upon user-specified input parameters.

Information and instructions on how to use the fire calculator

One of the most important things to note in using this calculator is that all growth rates (e.g. market returns and income growth rate) and values shown are done on a real basis, i.e. everything is done in current dollars.

Your Target Retirement Amount is based upon your expected annual retirement spending and your withdrawal rate.

FIRE Target amount = retirement spending / withdrawal rate

The choice of withdrawal rate is an important one. The withdrawal rate is defined as the percentage of your retirement savings that you withdraw when you start your retirement. The canonical retirement withdrawal rate is 4%. Click here to learn more about how withdrawal rates and historical simulations work. This means that you will withdraw 4% of your initial retirement balance annually (and adjusted for inflation). On a $1 million dollar retirement account, this amounts to $40,000 annually. To understand the risks of different withdrawal rates, see the 4% rule / safe withdrawal rate visualizer.

In addition to your initial level income and spending, you also have the ability to specify multiple income or expense streams over any specified number of years (based on age). This is helpful if you expect certain extra income sources or expenses to only occur for a finite amount of time (including one time payments), such as mortgage payments, child care costs, college tuition payments or an inheritance.

Your money (including the money you’ve already saved and the amount you save each year) is invested based upon your asset allocation and will grow based upon the following formula annually.

End of Year Savings = Previous Savings x (1 + GrowthRate) + AnnualSavings

The growth rate will vary based upon how much of your savings is invested in stocks vs bonds vs cash and the annual growth rate for each of these assets.

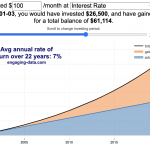

Your savings rate plays a large role in accumulating enough to retire and improving your savings rate can be done by reducing your annual spending and/or increasing your annual income.

Savings rate = (Annual (Post-tax) Income - Annual Spending) / Annual (Post-Tax) Income

The early retirement calculator determines how many years it takes to reach the FIRE Target.

- Fixed percentage: This mode requires you to enter the expected value for future real stock and bond returns (the default is the US historical average values from 1871 to 2015 of 8.1% and 2.4%). You can see how your retirement time depends on these rates of return.

- Historical cycles: This mode uses real stock and bond returns data from the last ~145 years and applies them sequentially to your savings annually to project their growth over time. Each of these chronological series of years starting in a different year is one historical cycle. Each cycle has a different series of stock/bond returns and thus has a different amount of money each year (even with the same annual savings profile).

- Monte Carlo simulation: This mode simulates thousands of possible sets of paths to meet your target and calculates the probability of different trajectories for your retirement investments. You can use the historical distribution of returns for your draws (8.1% real return for stocks and 2.4% for bonds) or you can specify a different average return for each set of assets. This enables you to run for optimistic or pessimistic scenarios.

.

When the calendar uses probabilistic outcomes from a series of model runs (i.e. the historical cycles approach and Monte Carlo simulation), the graph shows several bands, the 10th to 90th percentiles, the 25th to 75th percentiles and the median. Some definitions may be helpful for many folks here:

- 10th to 90th percentile – if you have a number of results or observations that you have put in order from smallest to largest, the 10th percentile is the result that is higher than 10% of the other results, while the 90th percentile is higher than 90% of the results. The range from 10th to 90th percentile encompasses 80% of the results and ignores the extreme outliers in the data.

- 25th to 75th percentile – similarly, ordering results or observations from smallest to largest, the 25th percentile is the result that is higher than 25% of the other results, while the 75th percentile is higher than 75% of the results. This range encompasses the middle 50% of the results and ignores the lowest and highest results.

- Median – the median is the data point that is in the middle of the ordered data; exactly half of the results are below and half are above.

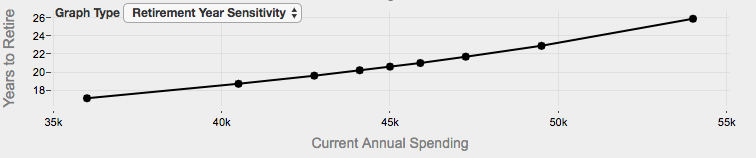

Sensitivity Analysis

A sensitivity analysis is also included to help you understand the implications of reducing (or increasing) your spending while saving up for retirement. There are two options for sensitivity:

- Current Spending Sensitivity – Sensitivity of retirement time to current spending. **Note, this sensitivity focuses on spending while saving up for retirement, not spending after retirement** The calculator runs different spending cases between -20% and +20% spending to show you how your time to retirement changes with these spending amounts.

- Stock Returns Sensitivity – Sensitivity of retirement time to stock market returns, which varies the user input stock market returns for the fixed and monte carlo cases between -60% and +60% returns.

When using the Historical cycles or Monte Carlo projection, you can view a histogram showing the distribution and variation in the number of years until retirement. Each of these individual runs has it’s own value for when your total invested savings surpasses the FIRE target.

When using the Historical cycles or Monte Carlo projection, you can view a histogram showing the distribution and variation in the number of years until retirement. Each of these individual runs has it’s own value for when your total invested savings surpasses the FIRE target.

While the frequency of events occurring in the past does not necessarily reflect the future probability, this distribution of outcomes gives a sense of the potential variation in number of years until retirement depending on whether there are a good or bad series of stock market returns

One of the key takeaways is that early on in your journey towards retirement, savings plays a larger role than investment returns. This highlights the importance of having a high savings rate if you would like to minimize the amount of time it takes to achieve your FIRE target.

I hope that is tool will be useful for anyone trying to achieve financial independence. As always, any comments, suggestions or feedback will be greatly appreciated.

Calculator Update – I added a button to generate a URL for a specific scenario that you can share with others.

UPDATE: September 2020: I’ve added the ability to add multiple additional income and expenses streams (with starting and ending dates). Since the calculations are all made in real dollars, these streams are assumed to change along with inflation.

Data source and Tools Historical Stock/Bond and Inflation data comes from Prof. Robert Shiller. Javascript, HTML and CSS are used to build the interface and javascript is used to calculate, process and aggregate the retirement balance results over all historical cycles and the results are graphed using Plot.ly javascript graphing library.

Privacy and Data statement: None of the information entered into the calculator is transmitted to our server or anywhere else. All of the data stays on your computer and all of the calculations are made within your browser (rather than on this site’s server).

52 Comments »

52 Responses to FIRE Calculator: When can I retire early?

Is the input field “Retirement Spending” with or without taxes?

Retirement spending does not include taxes, that is accounted for in the “Avg Tax Rate” field. You will need to withdraw more than the spending amount to pay for the taxes based on this rate.

This tool is amazing. Thank you so much for building and sharing this 💖

This FIRE calculator is a game changer! It’s so helpful to see how different variables affect my retirement timeline. I didn’t realize how much my expenses could impact my early retirement goals. Thanks for sharing this tool—definitely inspired to run my numbers!

It seems like the retirement spending need to include the mortgage amount else the fire target seems too low.

But the retirement spending should be reduced once the mortgage is over. How can I simulate this scenario?

Thank you for this nice simulator

I lumped all my expenses in one bucket whether it is a mortgage, food, loan payments, etc. I put my total income in the left and then my total expenses were income-everything that did not make it into an investment. So if I make 100,000 and I was only saving 5000 in my 401k each year then I spending $95,000 which includes my mortgage payment. In my scenario I pay off my mortgage a couple years before my fire date, so I added an income source equal to my mortgage payment starting the year I pay it off. I found that any income that came in after my FIRE date did not affect the calculations since the fire date is the end product.

“Extra Income” doesn’t appear to work. No matter what I type in, nothing changes.

On the right of “extra income”, there are two input boxes to specify the “Start Age” and “End Age” of the income. If your extra income starts after your retirement projection date then nothing will change if you add income. Try changing the start and end age to see if that works.

Can you use a different age to end at? Like if I think I’m going to live to 100 can I use 100 somehow in this calculator as the end?

The calculator isn’t designed to go to a specific age that you think you’ll live to. It shows you how long it’ll take you to save up a certain amount of money. If you want to see how long your retirement money will last, use the post-retirement calculator.

Post-Retirement FIRE Calculator: Will My Money Survive Early Retirement? Visualizing Longevity Risk

This is a great calculator. It would be even better if this took into account home equity and a fixed rate mortgage though.

Because there is a problem if you include your mortgage payments in your annual expense. The calculator will assume that your mortgage payments will rise with inflation, thus giving an overestimate of your retirement target. When in reality, this portion of your monthly expenses will be fixed and will benefit from inflation over time.

So what I ended up doing is subtracting the listing price of a new home from my savings and investments, and excluding mortgage payments from the annual expenses (while including property tax, home owner’s insurance etc). I assume that the money I kept aside equal to the home value will have a greater yield from a stock/bond allocation than the mortgage interest due on the amount.

The Monte Carlo simulation option seems to be reporting incorrectly when using the extra income option. It appears to double the extra income that is input.

What is the life expectancy in the calculations and could you please add a dropdown where we could update our life expectancy (I would guess this based on family members life expectancies)? This would change a lot on the calculations, as right now it says I can fire soon, but it would probably not cover for the remaining 20-30 years of my long life 🙂

Btw, best calculator I’ve come across so far! Super clear and seems quite accurate. Appreciate you putting this out here!

If you are interested in life expectancy and the likelihood of your savings covering you through a long retirement, you should check out the Rich, Broke or Dead calculator.

https://engaging-data.com/will-money-last-retire-early/

Hi, thank you for this calculator. I really like it.

Regarding inflation; what rate of inflation is being baked into the calculation to preserve purchasing power? (I apologize if it is listed somewhere, I scanned the page and can’t find the rate of inflation being used).

I know we should run various scenarios for rates of return as we can’t depend on the past performance to drive future expectations but as we are nearing end of 2020, what do the economic gurus say we should project for future realistic returns? I thought I read somewhere in September of this year that a more likely rate of return to project may be more like 7.1% for stock and 1.4% for bonds going forward (sorry I don’t have the source). Thoughts!

Thanks again for the calculator!

It looks like the way the estimate accounts for your estimated tax rate in retirement is incorrect. The way it should work: If your FIRE target (ignoring tax) is $1,000,000 and your estimated tax rate in retirement is 10%, then you need $1,111,111.11. For every $1 you withdraw, you keep $0.90, so to keep $1 you must withdraw $1.11; put another way, $1,111,111.11 * .90 is the target of $1,000,000. That is, PRETAXTARGET = AFTERTAXTARGET / (1 – TAXRATE).

The way it seems to work is that it adds the estimated tax rate as a percentage to the target, instead. (So if your FIRE target was $1,000,000 and your estimated tax rate in retirement is 10%, then it suggests you need $1,100,000.) That erroneous calculation would look like PRETAXTARGET = AFTERTAXTARGET * (1 + TAXRATE).

Yeah agreed. The tax calculation is incorrect. It’s off by about 1% for a 10% tax rate, which isn’t terrible, but it is notable and fixing it would increase my confidence in this tool.

Hey there! Awesome to see the update on adding those time-limited income and expense flows! Allowed me to account for a windfall from an asset becoming liquid and accounting for the expense of a child.

I think I’ve noticed a bug, or at least some weird behavior: changing the income growth rate back and forth between two numbers ends up producing inconsistent results. i.e., 4% -> 8.9 years, then 7% -> 8 years, then back to 4% -> 8.8 years, then back to 7% -> 7.9 years. I’ve seen this when planning out two different scenarios in the calc so it seems like a robust error, but here’s one where it happens: https://engaging-data.com/fire-calculator/?age=29&initsav=110000&spend=45000&initinc=120000&wr=4&ir=4&retspend=60000&stockpct=100&fixpct=0&cashpct=0&graph=mc&secgraph=0&stockrtn=8.1&bondrtn=2.4&MCstockrtn=7.1&MCbondrtn=2.4&tax=12&income=50,000&incstart=30&incend=30&expense=20,000&expstart=30&expend=50

The feature “to specify multiple income or expense streams over any specified number of years (based on age) ” is pretty cool. However, playing with the input there doesn’t seem to change the estimated Fire Target, nor does it change the estimated time to retirement. It does however reflect in the savings graph, but leaving the estimated time to retirement unchanged seems a little misleading.

Great calculator Christ with the update, would you be able to add an expense ratio section?

Great calculator. How can I add in a pension that I will have in 10 years?

[…] in order to maintain this lifestyle. A few calculators to demonstrate the concept here, here, and here. It should be noted: financial independence does NOT mean […]

This is the best tool on the internet. Please let it survive forever, I’d hate to lose it!

Hi,

Is it possible to also add in lifestyle increase. I see the annual spending piece doesnt increase at all and there’s no way of adding a percentage of increase on lifestyle. Is that possible?

Many thanks in advance!

Christian

Thanks for making this amazing calculator. I use it in almost every blog post with a FIRE calculation. I love the generate URL feature! A request: can you make an option to change the currency symbol shown? I am thinking Euro, Indian Rupee, AUD, SGD etc.

Love this calculator, but I like use the calculator at nesteggly because it can create URLs.

You can create URLs by pushing the “Generate URL” button then copy the URL box.

This doesn’t take into account social security or a pension does it ?

It’s missing a crucial component that the best retirement calculators have. The ability to introduce and calculate for a future lump sum distribution – e.g. inheritance or life insurance payout, in X number of years from now. Ditto re: Social Security. Is this or can this be factored in? Thanks.

Thanks for the calculator.

why does the tax rate default to 4%? isn’t the minimum about 15%?

No, the minimum tax rate is 0%. The tax rate is the average tax rate you see across all of your income. 15% is one of the marginal tax rates that is typical, but marginal rates only apply to a portion of your income, not all of it. See this tax calculator to see how much income you would need to have in order to have an average tax rate of 15% and what your average rate would be at your income level.

yeah, I had thought the same thing- mine defaulted to 7% – but about 15% tax rate seems more realistic. I pay over 30% now w/ state and federal so I can’t imagine less than 15%. But maybe I need to get a tax person?!

It will depend on how much you want to spend in retirement. Some FIRE folks can retire on $40,000/yr. If you are married, your fed tax rate can be around 5%. If you need $100,000/yr and are married, your average federal tax rate is closer to 10%.

plus state tax

“You can retire in -2.2 years at age 36.” I wish I could go back in time

[…] on Reddit that is better than the majority I have seen out there. I encourage you to take a look here. You can put in custom amounts for stock/bond allocation, current saving’s rate, age, taxes, and […]

Does the retirement spending factor in future inflation? For example $25,000 in 15 years has the same buying power as $16,000 or so today. If I need $25,000 in today’s dollars to retire I actually need to receive $38,000 or so in 15 years.

Yes spending is inflated into the future so that your purchasing power is more or less preserved.

Hi Chris,

How is the spending inflated for example if my FIRE target is $1million in today’s terms, how is it calculating the value of what a $1million feels like in the future. For example inflation can make that feel like $500,000 in roughly 15 years. Just want to gauge how you have inflated spending into the future?

Many thanks!

Great calculator!

Will there be a way to adjust the ‘spending’ amount against earning? E.g. as a percentage in relation to income, or just have a fixed saving rate as income is indexed.

Is income growth just what we expect our yearly raises to be? My average annual raise for the last 3 years has been 8.5% – is that what goes in here? When I use that, the years to retirement seems a little too low from other calculators I’ve seen.

Thanks for this work on this.

Just so I’m clear, results are in today’s dollars. This, if results show a retirement value of 1 million, i assume it’d actually be higher that year. Just want to make sure I’m not overestimating this, as this calculator seems more generous than Personal Capital’s retirement calculators, for example.

Thanks for the mobile friendly update – works great!

I think this calculator gave me my favorite response in a calc I’ve ever seen:

“You can retire in -0.5 years at age 35”

Awesome work!

I had the same response, time-wise. I can retire in 6 months.

It’s a shame I’m 20 years older!!!!

This is great, thank you!

A few questions:

1. How to incorporate college fees for children?

2. How do i capture the potential value of my home? For example, if I live in a large city and estimate I can sell it at 1M in 20 years, and move to a low cost area?

Wonderful job with the calculator. I appreciate the work you put into it.

Very quick and easy to use when I want to see a “what if” type scenario. Just bookmarked. Thanks again!

How would rental income be used in this situation? Would the equity in the rentals be included in your investment amount? Thanks!

You could include it into your net rental income (minus expenses) or you could subtract it from your expenses. Either way will work. If you believe it will grow faster than inflation you probably should put it in income so you can apply the income growth rate.

You shouldn’t put the equity into your savings as you won’t be earning a return on that that you can live on.

Great calculator, thanks for putting the effort into this!

Very well done, thank you!

[…] 2. When Can I Retire? Early Retirement Calculator […]